Artículo de noticias

Barómetro Q1 QIMA 2024

25 ene 2024

BARÓMETRO Q1 2024: Resumen de 2023: ¿El nearshoring como opción principal de China?

Entre la recesión económica mundial y las tensiones geopolíticas, el 2023 ejerció una presión significativa sobre las marcas y los minoristas para que optimizaran sus costes y aseguraran sus cadenas de suministro. Para muchos, esto significó volver a centrar su atención en China, aumentar los esfuerzos de nearshoring o seguir ambas estrategias simultáneamente. Mientras tanto, los continuos retos en la visibilidad de la cadena de suministro indican que las empresas están lejos de estar preparadas para la inminente ola de legislación ESG que entrará en vigor en los próximos meses. Este informe barómetro, basado en datos internos de QIMA y en los resultados de nuestra encuesta a más de 800 empresas con cadenas de suministro internacionales, ofrece una retrospectiva de 2023 en materia de contratación y expectativas para el próximo año.

El 2023 marca el retorno de China como fuente de adquisición

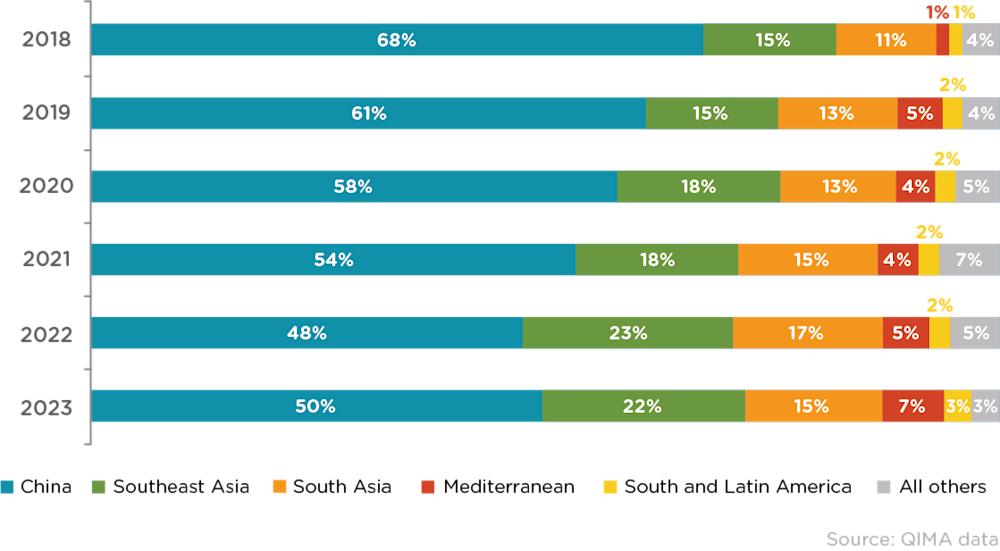

Después de varios años turbulentos de interrupciones relacionadas con la pandemia y desafíos logísticos, el abastecimiento de China parece haber consolidado su recuperación en 2023. Los datos de QIMA muestran que la demanda de inspecciones y auditorías de China entre los compradores con sede en EE. UU. y la UE ha aumentado un 5.4% interanual en 2023, mientras que la cuota relativa de China en las carteras de proveedores de estos compradores ha aumentado por primera vez desde 2018 , una tendencia destacada en nuestro barómetro del cuarto trimestre de 2013, que se ha fortalecido aún más desde entonces.

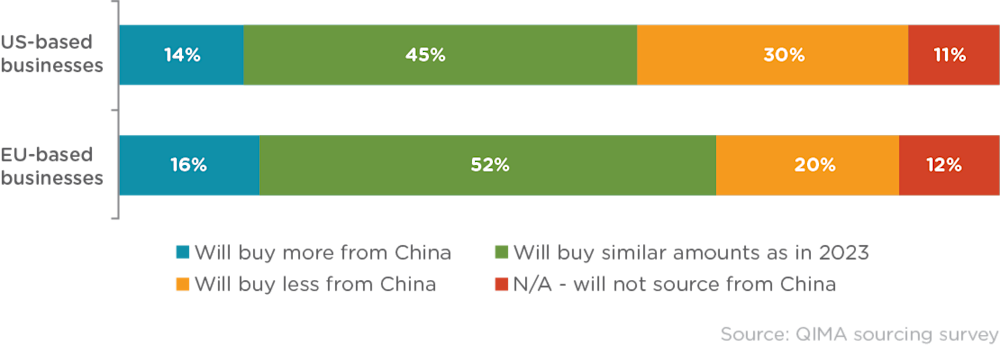

A medida que nos adentramos en 2024, hay margen para el optimismo en lo que respecta a la contratación en China, tanto a escala mundial como en Occidente. En la encuesta de QIMA, el 59% de los encuestados con sede en EE.UU. y el 68% de los que tienen su sede en la UE informaron de planes para mantener o aumentar los volúmenes de negocio con proveedores chinos. Además, se espera que los mercados emergentes sigan desempeñando un papel importante para China: por ejemplo, los datos de QIMA muestran que la demanda de inspección y auditoría de las empresas con sede en América Latina y del Sur aumentó un +17% interanual en 2023. Si bien los mercados nacionales contribuyen a este crecimiento, una parte sustancial del mismo puede vincularse a los crecientes volúmenes de nearshoring por parte de las marcas estadounidenses, lo que impulsa la demanda de materias primas y componentes chinos entre las empresas locales.

Sin embargo, es importante recordar que durante los últimos cinco años, el panorama de la cadena de suministro mundial se ha vuelto cada vez más volátil, y el impacto de la geopolítica en el comercio es mayor que nunca. Teniendo esto en cuenta, cualquier predicción para el abastecimiento de China en 2024 debe considerar que las elecciones presidenciales de EE. UU. tienen el potencial de remodelar aún más la relación comercial entre EE. UU. y China.

Fig. C1: Principales mercados proveedores de compradores de EE.UU. y la UE (cuota relativa en volúmenes de aprovisionamiento)

Fig. C2: "¿Cuántos negocios tiene previsto hacer con proveedores chinos en 2024, en comparación con 2023?"

El nearshoring avanza, desviando mayores volúmenes de compra de mercados internacionales

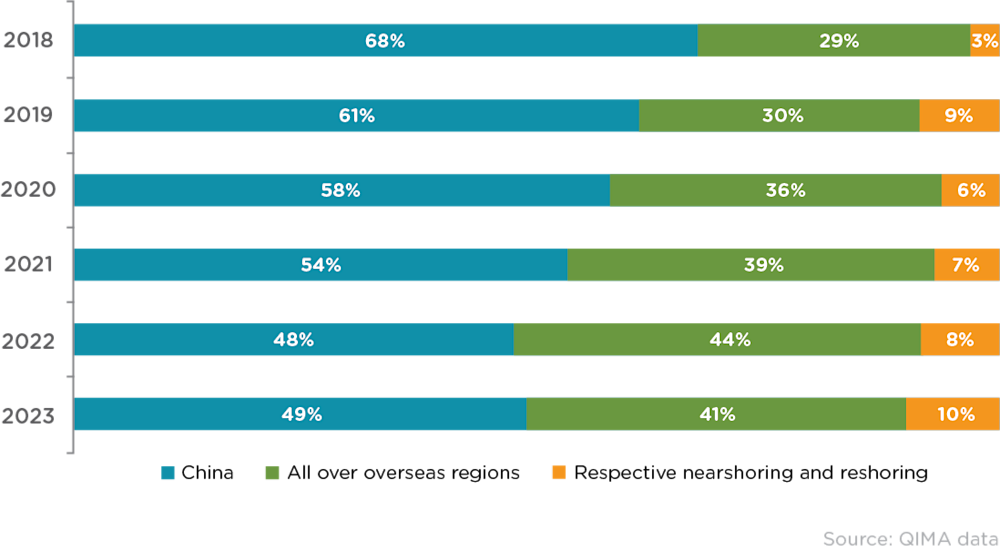

La popularidad del nearshoring y el reshoring ha seguido creciendo a lo largo de 2023, a tal punto que los volúmenes abastecidos desde el país de origen y las regiones cercanas están aumentando a expensas de los mercados de proveedores internacionales (excepto China). Los datos de QIMA sobre la demanda de inspección y auditoría para 2023 muestran un repunte en la cuota relativa de las respectivas regiones de nearshoring y reshoring entre los compradores con sede en EE. UU. y la UE, que ahora representan un total del 10% de sus compras.

Además, mientras que en el pasado las empresas europeas se inclinaban más por comprar a proveedores más cercanos, los resultados de la encuesta sobre contratación de QIMA indican que los compradores con sede en EE. UU. están ahora igualmente interesados en el reshoring y nearshoring . Los datos de QIMA sobre la demanda de inspecciones y auditorías corroboran esta afirmación: México, que superó a China como el socio comercial número uno de Estados Unidos este año, vio cómo la demanda de inspecciones y auditorías se expandía un +16% interanual en 2023.

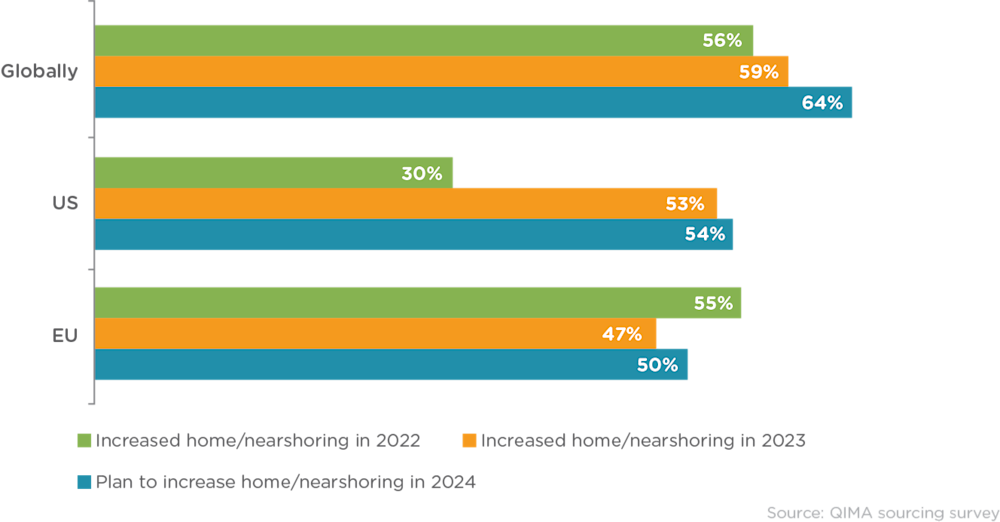

Hasta ahora, la tendencia hacia el aumento del nearshoring y reshoring no muestra signos de desaceleración. De cara al futuro, el 54 % de los encuestados con sede en EE. UU. y el 50 % de los encuestados con sede en la UE informaron de sus planes de abastecerse más de proveedores de su región de origen y regiones cercanas en 2024.

Figura N1: Cuota relativa de las regiones de origen e internacionales en la contratación de compradores de EE. UU. y de la UE.

Fig. N2: Evolución del interés de los compradores por el nearshoring y el reshoring, 2022-2024 (por ubicación de la sede central de los encuestados).

Los mercados de proveedores asiáticos luchan en el contexto de una demanda mundial más débil

Tras un periodo de expansión explosiva en 2022, el abastecimiento en Asia del Sur experimentó un año más lento en 2023. Bangladesh, en particular, se enfrentó a desafíos con los conflictos salariales y la crisis política en curso que paralizó grandes franjas de fabricación en el cuarto trimestre. Mientras tanto, la India, aunque sigue siendo una de las principales opciones para el abastecimiento en el extranjero entre los encuestados por QIMA, vio ralentizarse el ritmo de expansión de nuevos negocios. Entre los factores que explican este parón se encuentran las políticas proteccionistas del país, que al parecer han influido en las recientes decisiones sobre la cadena de suministro tomadas por las principales empresas occidentales de . Con los dos principales mercados proveedores del sur de Asia en retroceso en 2023, los datos de QIMA muestran que la demanda de inspecciones y auditorías en la región retrocede a los niveles de 2021.

En comparación, al Sudeste Asiático le fue mejor, pero el ritmo de crecimiento se vio frenado por el debilitamiento de la demanda mundial. Camboya se situó a la cabeza, según los datos de QIMA, con una demanda de inspección y auditoría del 11 % interanual en 2023, lo que supuso un tercer año consecutivo de expansión de dos dígitos, mientras que Vietnam, Indonesia y Filipinas registraron un crecimiento interanual en torno al 5 %.

El cumplimiento ético está relacionado con la madurez de la región de aprovisionamiento, como muestran los datos de auditoría

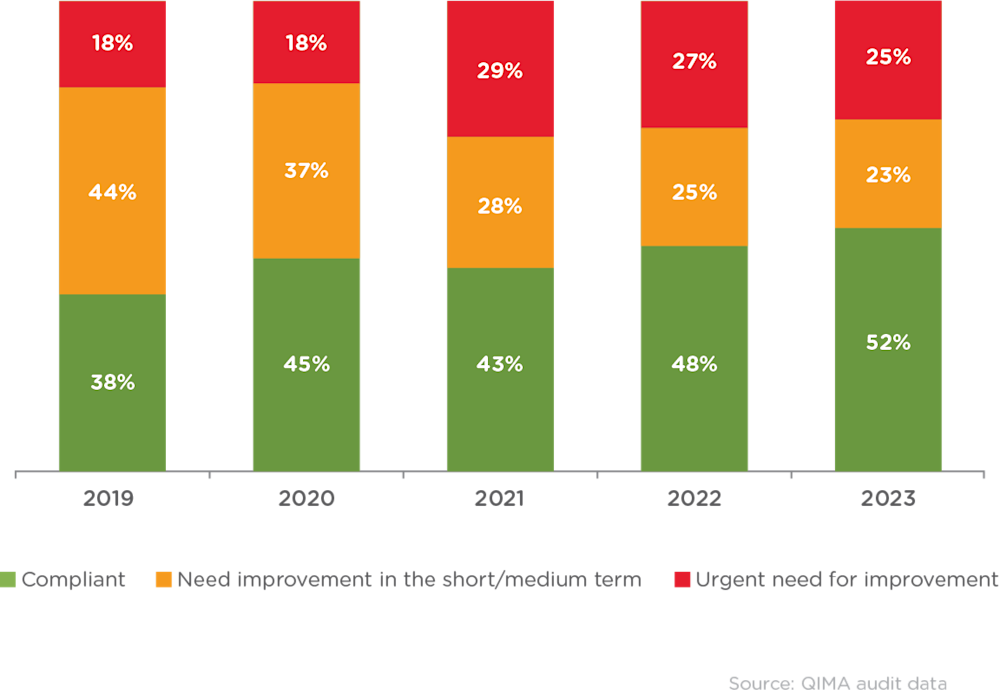

Al ser encuestados por QIMA, casi dos tercios de los encuestados afirmaron que el cumplimiento por parte de los proveedores se había vuelto más importante para ellos en comparación con hace un año, y el 70 % declaró tener en cuenta al menos un factor ESG en sus decisiones de aprovisionamiento. Sin embargo, los datos de las auditorías sobre el terreno revelaron que los avances en materia de cumplimiento ético fueron lentos en 2023. A una cuarta parte de las fábricas inspeccionadas se les asignó una clasificación "roja" que indicaba la necesidad de una reparación urgente (frente al 27% en 2022). Los problemas más acuciantes fueron la salud y la seguridad y los horarios de trabajo y los salarios, que representaron el 31% y el 36% de todos los incumplimientos críticos detectados por los auditores de QIMA en 2023, respectivamente.

La escasa visibilidad de la cadena de suministro puede ser la causa de la brecha entre las estrategias ESG y su aplicación real: solo el 16% de los encuestados por QIMA declararon conocer a todos sus proveedores (en todos los niveles), y casi un tercio de las empresas conocían a menos del 50% de su cadena de suministro.

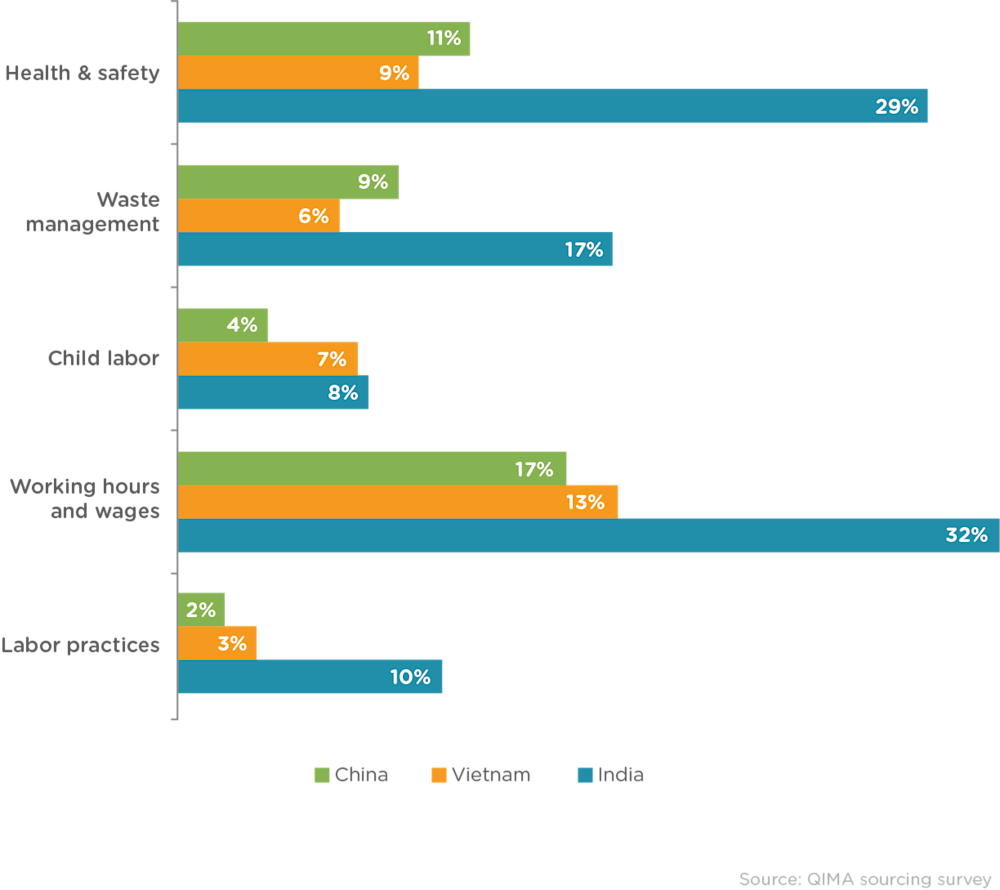

Los datos de auditoría por países también sugieren una correlación positiva entre el cumplimiento ético y la madurez de la región de aprovisionamiento. Por ejemplo, en China, los auditores de QIMA registraron infracciones críticas en materia de salud y seguridad en el 11% de las fábricas auditadas, mientras que en la India esa cifra fue del 29%. Este patrón se observó en todos los aspectos del cumplimiento ético cubiertos por las auditorías de QIMA, incluido el trabajo infantil, que era dos veces más probable encontrar en las fábricas de Vietnam y la India que en China.

Fig. E1: Evolución de las clasificaciones de fábricas asignadas por las auditorías éticas, 2019-2023 (medias mundiales).

Fig. E2: Porcentaje de auditorías en las que se descubrieron infracciones críticas en las categorías indicadas en 2023 (comparación por países).

Los principales retos de abastecimiento de 2023 se extienden a 2024: las marcas se preparan para un año difícil

La lista de retos de la cadena de suministro de 2023, según la clasificación de los encuestados por QIMA, estaba dominada por el aumento de los costes, las fluctuaciones de la demanda y las tensiones geopolíticas, factores todos ellos que se espera que persistan en 2024. A medida que disminuya la disponibilidad de capital circulante y la inflación afecte al gasto de los consumidores, las marcas y los minoristas se enfrentarán a una mayor presión para optimizar los costes y mitigar los riesgos, siendo probablemente el nearshoring una de las estrategias empleadas. El despliegue en curso de la normativa ESG presenta un reto adicional, haciendo hincapié en la necesidad de una mayor visibilidad de la cadena de suministro

Contacto de prensa

Correo electrónico: press@qima.com

Compartir en